50/30/20 Rule Explained for Nigerians: A Practical Guide to Smarter Budgeting

By MetroNub Staff

The 50/30/20 rule is one of the most popular personal finance frameworks in the world—but how well does it actually work for Nigerians dealing with rising living costs, inflation, and irregular income?

In this detailed guide, we break down the 50/30/20 rule explained for Nigerians, how it works, where it fits the Nigerian financial reality, and whether it’s still a practical budgeting strategy in 2026.

Introduction: Why Budgeting Matters More Than Ever in Nigeria

If you live in Nigeria, you already know that managing money is not just about earning—it’s about survival, planning, and adapting. With fluctuating fuel prices, food inflation, rent pressure, and unpredictable income streams, budgeting has become essential rather than optional.

That’s where the 50/30/20 budgeting rule comes in. It promises a simple structure to manage your income without stress or complex accounting tools. But does it really work in the Nigerian economy?

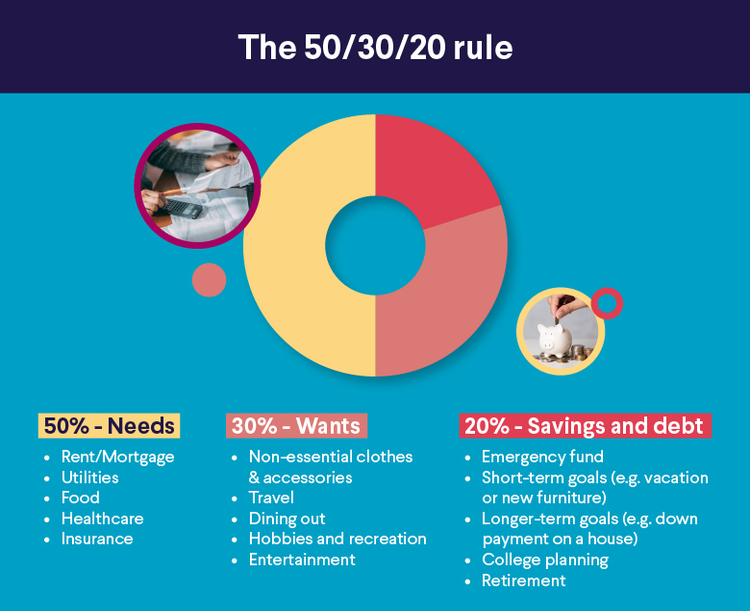

What Is the 50/30/20 Rule?

The 50/30/20 rule is a simple budgeting method that divides your after-tax income into three categories:

- 50% Needs – essentials for survival

- 30% Wants – lifestyle and non-essential spending

- 20% Savings & Debt Repayment – financial growth and security

It was popularized by U.S. Senator Elizabeth Warren as a straightforward way for individuals to gain control over their finances.

Breaking It Down Further

- Needs (50%): Rent, food, transportation, utilities, school fees, basic healthcare

- Wants (30%): Eating out, Netflix subscription, fashion, gadgets, entertainment

- Savings (20%): Emergency fund, investments, savings accounts, loan repayment

How the 50/30/20 Rule Applies to Nigerians

While the rule is simple on paper, applying it in Nigeria can be challenging due to economic realities.

1. High Cost of Living

In cities like Lagos, Abuja, and Port Harcourt, rent alone can consume more than 50% of income for many people. Transportation and food inflation further stretch the “needs” category beyond the recommended limit.

2. Irregular Income

Many Nigerians work in the informal sector, freelancing, or small businesses where income is not fixed monthly. This makes strict percentage budgeting harder to maintain consistently.

3. Currency Inflation Pressure

With inflation affecting food, fuel, and imported goods, budgeting categories often shift unpredictably, making rigid financial rules difficult to follow.

Does the 50/30/20 Rule Really Work in Nigeria?

Short answer: Yes—but with modifications.

The 50/30/20 rule works best as a guideline, not a strict law. For Nigerians, it often needs adjustment to reflect reality.

Why It Works

- It simplifies money management

- Encourages disciplined saving habits

- Helps reduce unnecessary spending

- Creates financial awareness

Why It May Not Work Directly

- Basic needs often exceed 50%

- Low-income earners struggle to save 20%

- Wants category may be unrealistic for tight budgets

Real-Life Example of the 50/30/20 Rule in Nigeria

Let’s assume a monthly income of ₦300,000:

- Needs (50%) = ₦150,000

- Wants (30%) = ₦90,000

- Savings (20%) = ₦60,000

Now compare this to reality:

- Rent in Lagos may be ₦100,000+

- Transport + feeding may exceed ₦80,000

- School fees or family support adds extra pressure

This shows that the "needs" category can easily exceed 50%, making adjustments necessary.

Modified 50/30/20 Rule for Nigerians

To make this budgeting system more realistic, many financial experts suggest adapting it:

Option 1: 60/20/20 Rule

- 60% Needs

- 20% Wants

- 20% Savings

Option 2: 70/20/10 Rule (Low Income Earners)

- 70% Needs

- 20% Wants

- 10% Savings

Option 3: 50/40/10 Rule (Lifestyle Balanced)

- 50% Needs

- 40% Wants (flexible lifestyle)

- 10% Savings

Practical Tips to Make the 50/30/20 Rule Work in Nigeria

1. Track Every Expense

You cannot manage what you don’t measure. Use budgeting apps or simple notebooks to track spending daily.

2. Prioritize Needs Ruthlessly

Differentiate between true needs (food, rent) and disguised wants (premium subscriptions, unnecessary upgrades).

3. Automate Savings

Transfer savings immediately after income arrives to avoid spending temptation.

4. Build an Emergency Fund

Even if you start small, aim for 3–6 months of expenses for financial stability.

5. Reduce Lifestyle Inflation

As income increases, avoid increasing spending at the same rate. Instead, boost savings.

Common Mistakes Nigerians Make With Budgeting

- Ignoring savings entirely

- Overestimating income stability

- Mixing business and personal finances

- Failing to adjust budget during inflation

- Not planning for emergencies

Benefits of the 50/30/20 Rule

Despite its limitations, the rule offers significant advantages:

- Simplicity: Easy to understand and apply

- Financial discipline: Encourages structured spending

- Goal setting: Helps you prioritize savings

- Stress reduction: Removes guesswork from money management

Is the 50/30/20 Rule Enough for Wealth Building in Nigeria?

On its own, the 50/30/20 rule is not a wealth-building strategy—it is a budgeting framework. To build wealth in Nigeria, you need to combine it with:

- Side hustles or multiple income streams

- Investments (stocks, real estate, mutual funds)

- Skill development for higher earning potential

Think of it as a foundation, not the entire house.

Final Verdict: Should Nigerians Use the 50/30/20 Rule?

The 50/30/20 rule explained for Nigerians is best seen as a flexible guideline rather than a strict formula. It works well for financial awareness and discipline, but must be adapted to local realities like inflation, rent pressure, and irregular income.

If used correctly—with modifications—it can help Nigerians take control of their finances, reduce debt, and start building savings consistently.

Bottom line: It works, but only if you make it work for your reality—not the other way around.

Conclusion

Financial stability in Nigeria requires more than just earning money—it requires strategy, discipline, and adaptability. The 50/30/20 rule is a powerful starting point, but not a one-size-fits-all solution.

By adjusting the percentages, tracking expenses, and building consistent saving habits, you can turn this simple rule into a practical financial tool that works even in a challenging economy.